Page 87 - JTC-Annual Report-2025-Eng

P. 87

JTC Logistics Transportation & Stevedoring Company K.S.C.P

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

As at December 31, 2025

(All amounts are in Kuwaiti Dinars)

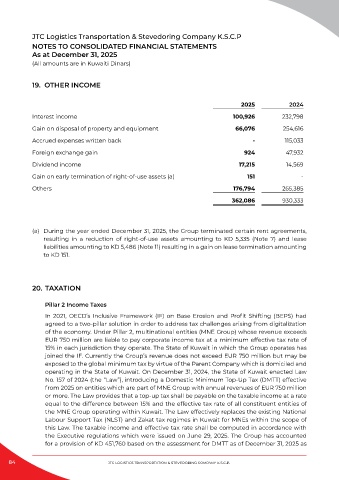

19. OTHER INCOME

2025 2024

Interest income 100,926 232,798

Gain on disposal of property and equipment 66,076 254,616

Accrued expenses written back - 115,033

Foreign exchange gain 924 47,932

Dividend income 17,215 14,569

Gain on early termination of right-of-use assets (a) 151 -

Others 176,794 265,385

362,086 930,333

(a) During the year ended December 31, 2025, the Group terminated certain rent agreements,

resulting in a reduction of right-of-use assets amounting to KD 5,335 (Note 7) and lease

liabilities amounting to KD 5,486 (Note 11) resulting in a gain on lease termination amounting

to KD 151.

20. TAXATION

Pillar 2 Income Taxes

In 2021, OECD’s Inclusive Framework (IF) on Base Erosion and Profit Shifting (BEPS) had

agreed to a two-pillar solution in order to address tax challenges arising from digitalization

of the economy. Under Pillar 2, multinational entities (MNE Group) whose revenue exceeds

EUR 750 million are liable to pay corporate income tax at a minimum effective tax rate of

15% in each jurisdiction they operate. The State of Kuwait in which the Group operates has

joined the IF. Currently the Group’s revenue does not exceed EUR 750 million but may be

exposed to the global minimum tax by virtue of the Parent Company which is domiciled and

operating in the State of Kuwait. On December 31, 2024, the State of Kuwait enacted Law

No. 157 of 2024 (the “Law”), introducing a Domestic Minimum Top-Up Tax (DMTT) effective

from 2025 on entities which are part of MNE Group with annual revenues of EUR 750 million

or more. The Law provides that a top-up tax shall be payable on the taxable income at a rate

equal to the difference between 15% and the effective tax rate of all constituent entities of

the MNE Group operating within Kuwait. The Law effectively replaces the existing National

Labour Support Tax (NLST) and Zakat tax regimes in Kuwait for MNEs within the scope of

this Law. The taxable income and effective tax rate shall be computed in accordance with

the Executive regulations which were issued on June 29, 2025. The Group has accounted

for a provision of KD 451,760 based on the assessment for DMTT as of December 31, 2025 as

84 JTC LogisTiCs TransporTaTion & sTevedoring Company K.s.C.p.